- No rate cuts this time, the interest rate remains 4.25%-4.5%.

- Rate Forecast Unchanged. The Fed projects the federal funds rate at 3.9% by the end of 2025 and 3.4% by the end of 2026, in line with December estimates.

- Monetary Policy Outlook. The Fed remains cautious, assessing economic data before adjusting rates further.

- Balance Sheet Reduction. The pace of the balance sheet decline will be slowed.

- Treasury Redemptions Adjusted. Monthly Treasury redemptions reduced from $25B to $5B, while agency securities cap remains unchanged to maintain market stability.

- Economic Growth. GDP grew 2.3% in Q4 2024, but consumer spending is moderating.

- GDP Forecast. Expected to grow 1.7% in 2025 and slightly below 2% in the following years.

- Labor Market. Solid job growth, averaging 200,000 new jobs per month over the last three months.

- Unemployment Rate. Remains low at 4.1%, projected to rise to 4.4% by year-end and 4.3% over the next two years.

- Labor Market Balance. Low firing and hiring trends have stabilized over the past 6–8 months.

- Inflation Trends. Inflation eased over the past two years but remains slightly above target.

- PCE Inflation. 2.5% over the past year, with core PCE (excluding food & energy) at 2.8%.

- Inflation Projection. 2.7% in 2025, 2.2% in 2026, reaching the 2% target by 2027.

- Inflation Volatility. Two months of higher-than-expected goods inflation, possibly temporary noise or early tariff impact.

- Tariffs and Inflation Impact. Recent inflation increases are partially linked to tariffs, but the exact contribution remains uncertain.

- Consumer Confidence Divergence. Surveys indicate high uncertainty, but hard economic data remains strong.

- Economic Uncertainty. Tariffs and policy changes (immigration, fiscal policy, regulation) contribute to uncertainty.

- New Administration’s Impact. Too early to see significant economic effects, though some localized layoffs were observed.

- Historical Tariff Effects. Market-based inflation reactions seen before, e.g., washing machine prices spiking after past tariffs.

March FOMC meeting is on – let’s dive into the key points and comments from Jerome Powell about the CPI, PPI, and other indicators that will influence the global economy and market – while the core question without surprises and we will see no rate cuts this time, the interest rate is still 4.25-4.5.

How much of the higher inflation forecast for this year is due to tariffs?

“That’s going to be very difficult to assess precisely… Some of it, a good part of it, is coming from tariffs. We will work to separate non-tariff inflation from tariff-related inflation.”

Does the Fed see the current inflation spike as transitory?

“It can be appropriate to look through inflation if it is going to fade quickly without action from us. That will depend on how fast tariff-related inflation moves through and whether long-term inflation expectations remain stable.”

The Fed’s inflation projections remain largely unchanged. Does this mean you see no real signal in recent inflation data and view it as transitory?

“I think that’s kind of the case. But as I said, we really can’t know yet. We have to see how things actually play out. The fact that there wasn’t much change is partly because growth and higher inflation offset each other, and also, frankly, there is some inertia when making policy changes in a highly uncertain environment.”

Given the increase in certain inflation expectation measures, has your confidence in long-term inflation expectations being well-anchored changed?

“In the short term, we see inflation expectations rising widely across different measures. But if you look at longer-term expectations, whether survey-based or market-based, they remain stable. We do not take anything for granted and will watch closely.”

How much weight do you place on the deterioration in consumer confidence? Could it be a leading indicator for economic weakness?

“Consumer sentiment is moderating, but the hard data—unemployment at 4.1%, healthy job creation, and solid consumer spending—remains strong. We acknowledge the uncertainty, but historically, sentiment and actual economic activity have not always aligned.”

Recent inflation spikes have started in goods but previously spread to services like haircuts and daycare. Why isn’t the Fed reacting more aggressively this time?

“If an inflation impulse is going to go away on its own, it is not the right policy to tighten unnecessarily. We are well aware of what happened with pandemic inflation, but this is a different situation.”

What is your stance on balancing higher prices and weaker growth? Will the Fed prioritize inflation control?

“We have two goals—maximum employment and price stability. In situations where these goals are in tension, we assess how far each is from target and how long it will take to return to equilibrium. That’s not the situation we are in right now.”

What the probability of a recession. Does the Fed see an increased recession risk?

“There is always an unconditional probability of a recession. Outside forecasts have raised recession probabilities somewhat, but they remain within historical norms. We do not currently forecast a recession.”

Layoffs are rising in some sectors. Is this a concern for the broader labor market?

“Layoffs remain localized and have not yet had a significant national impact. The labor market is still in balance. We are monitoring developments closely.”

Hiring has slowed, but firing remains low. What does this indicate?

“We’ve had a low hiring, low firing situation for the past 6–8 months. This suggests a labor market in balance, but we are watching carefully for any shifts.”

Have the new administration’s policies begun to impact economic data?

“It’s still too early to assess. Some layoffs are happening, but at the national level, they are not yet significant. We will have more clarity as the data unfolds.”

The Fed has seen two unexpectedly high inflation readings in the past two months. What is behind this?

“It’s hard to pinpoint, but it could be noise, or it could be an early response to tariffs. These effects can be indirect and difficult to track, as we’ve seen in past tariff rounds, such as with washing machines.”

Could waiting for more clarity on fiscal and trade policies put the Fed behind the curve in responding to a downturn?

“We are aware of the risks of waiting too long, but we believe it is the right time to pause and gather more data. Our current stance allows us to respond appropriately if needed.”

Do recent firings at the Trade Commission threaten the Fed’s independence?

“I answered that question some time ago, and I have no desire to change that answer. I have nothing for you on that today.”

The University of Michigan survey showed rising long-term inflation expectations. Is the Fed discounting that data?

“We look at all inflation expectation measures, but this one is an outlier compared to market-based and other survey data. We take note of it but consider the full range of indicators.”

Does the Fed believe it can effectively track policy impacts despite high uncertainty?

“Yes, we will assess the economic implications as policy changes are implemented and adapt as necessary.”

Could uncertainty around fiscal policies make it harder for the Fed to act in a timely manner?

“We are monitoring economic conditions closely and will use our tools to foster achievement of our goals in a timely way.”

Given the uncertainty in economic policy, do you believe the Fed can still effectively assess the situation?

“Yes, we will assess the economic implications as policy changes are implemented and adapt as necessary.”

How do you distinguish between noise and signal in inflation data?

“It’s just a way of saying that things are uncertain. The news is full of developments—tariffs being put on, taken off, things like that. Some of that is noise in the sense that it’s not telling you much. You try to extract the signal from that, which is the actual effect on economic activity, inflation, and unemployment.”

Is it possible to definitively determine how much of the recent inflation spike is due to tariffs?

“We had high readings for goods inflation after a period where readings were averaging close to zero. You have to ask, did it come from tariffs? It’s very hard to scientifically go back and match up those increases and say, yes, I can prove that’s the cause—but it kind of has to be, to some extent. Some of it could be erratic readings that later reverse. I think in a couple of months we’ll have a better idea.”

Consumer sentiment has dropped significantly, but you say the economy remains strong. What is your message to consumers who don’t feel that strength?

“Consumers are looking at their grocery bills. Inflation raised prices to a higher level, and people are unhappy about that. They’re not wrong to be unhappy—things cost more. That’s been a major reason why people feel negatively about the economy, even though the fundamentals—growth, inflation moving lower, unemployment—look solid.”

Given that inflation is projected to be higher for longer, does this mean you see an economic slowdown as a real risk?

“We are projecting broadly weaker growth but also slightly higher inflation, and they kind of balance each other out. It’s not a big enough shift in our forecast to meaningfully change policy. The second factor is the high uncertainty—we are in touch with businesses and households, and while sentiment has declined, economic activity has not. We are watching carefully.”

Are you still projecting rate cuts this year?

“We are positioned to wait for further clarity. The data will determine our decisions.”

Can you clarify what part of the inflation increase is due to tariffs—existing ones or anticipated ones?

“We know tariffs are coming in. Every forecaster has inflation rising this year in both core PCE and CPI—without exception. I can’t tell you exactly how much of that is tariffs, but it’s a factor.”

Did the decision to slow the balance sheet reduction have anything to do with expectations around the debt ceiling?

“The flow in and out of the Treasury General Account (TGA) got us thinking about it, but ultimately, we came to the view that this was a good time to slow the runoff. Cutting the pace roughly in half extends the process over a longer period, which makes sense. This action has no implications for monetary policy or the ultimate size of the balance sheet.”

Do you still believe inflation expectations remain well-anchored?

“Yes. We are watching short-term inflation expectations carefully, but longer-term expectations remain stable. That’s true in both market-based and survey-based measures.”

How do you assess the labor market, particularly in relation to government jobs?

“The labor market remains strong. We don’t have policies that address different types of employment—those are government decisions—but we continue to monitor labor market trends closely.”

Some indicators suggest rising risks to growth, including stock market volatility, slowing housing sales, and declining confidence. How confident are you that the Fed is well-positioned?

“We are well-positioned in the sense that we have flexibility to move in either direction. Forecasting is always difficult, and right now, uncertainty is particularly high. We are not in a hurry to move—we are watching for clarity.”

Would you be surprised if conditions required a policy pivot?

“We are not going to be in a hurry to move. We will wait for greater clarity.”

The Fed removed the line that risks to employment and inflation are ‘roughly balanced.’ Does this mean you are now more concerned about one or the other?

“No, it doesn’t. Sometimes, small language changes are made for clarity, but we continue to assess both risks. Many participants in the SEP raised their estimate of risks to growth and employment, but that does not mean we are shifting our approach at this time.”

Are you concerned that your previous remarks unsettled the markets?

“Markets react to data and to our communications, and that’s part of the process. We aim to be as clear and transparent as possible about our policy stance, and we remain focused on our dual mandate. We don’t set policy based on market moves, but we do take financial conditions into account as we assess the broader economy.”

Do you think that initiatives like DOGE’s plan to use saved funds to pay dividends to citizens could have any impact on economic stability?

“I’m not familiar with that specific proposal, but in general, fiscal decisions are outside our purview. Our focus remains on monetary policy, price stability, and maximum employment. How governments choose to allocate resources is a matter for elected officials and policymakers.”

Was the decision to slow QT (quantitative tightening) meant to be a temporary measure due to the debt ceiling, or is it a broader adjustment?

“The original discussion was provoked by the TGA flows, but what we came up with was broader than that. It does address that issue, but it also fits in well with our principles, our plans, and the things we’ve done before—the things we said we would do. That’s why it had pretty strong support. It’s not about policy or the size of the balance sheet; it’s just a common-sense adjustment as we get closer and closer. Let’s slow down a little bit, so we can be more confident we’re getting where we need to be.”

Will the pace of balance sheet reduction be regained once the debt ceiling issue is resolved?

“It really came together very strongly in favor of this move. Slowing down the path effectively ensures that the process remains smooth as we get closer to our goals. We think this was the right decision, and it aligns with our broader approach.”

Also, it’s too early to tell how the markets reacted, but in the first minutes after Jerome Powell’s speech, Bitcoin showed a slight rise from $85K to $85.2K, although just before the FOMC meeting we saw from $85.8K to $85.4K and even to $85K.

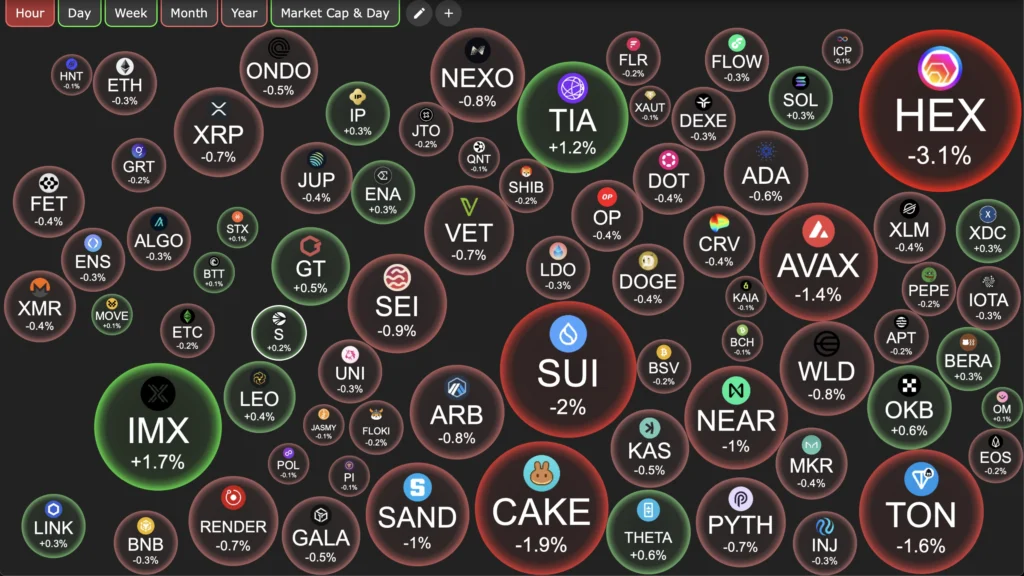

Overall we see short-term gains on all key cryptocurrencies, for example, SOL +1.9%, HBAR +1.6%, while DOGE outperformed even them with +1.9%, and even better performing SUI +2%, TAO +2.4% and IMX +3%. However, it remains to be seen whether this general trend will hold in general and even more so in each individual case.

However, bit later we can see as many of them roll back, and it remains to be seen whether this general trend will hold and even more so in each individual case.

Stay tuned for updates, be adaptive in the rapidly evolving financial and crypto landscape, and keep your strategy grounded, balanced, and beneficial.

The information provided in this article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Any actions you take based on the information provided are solely at your own risk. We are not responsible for any financial losses, damages, or consequences resulting from your use of this content. Always conduct your own research and consult a qualified financial advisor before making any investment decisions. Read more